In an unstable economic context, marked with price increases, financial uncertainty and salaries that do not keep step by step, efficient management management is a priority. For many Romanians, low incomes seem to be an obstacle for a balanced financial life. However, there are practical methods that, adapted intelligently, can bring orders to financial chaos. One of the most accessible and efficient methods is the 50/30/20 rule. Find out what this rule involves, how you can adapt it if you have a low income and how to apply it step by step, without giving up your goals.

What is the rule 50/30/20?

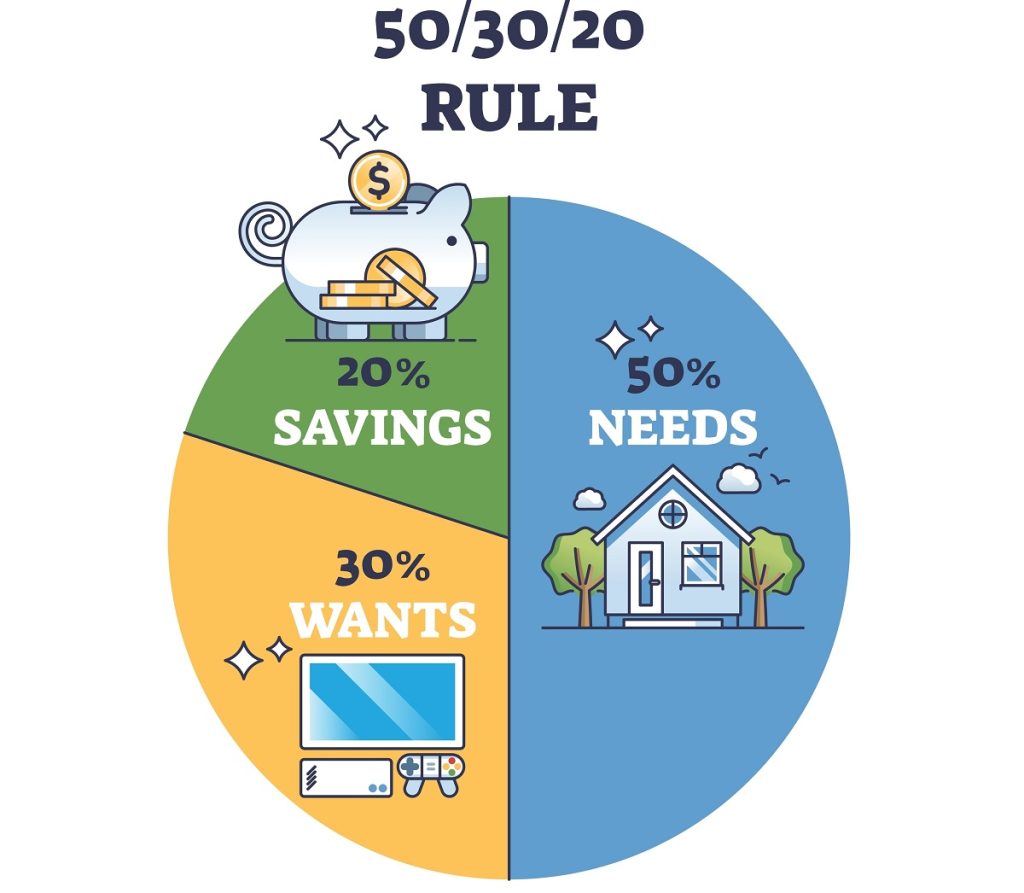

The 50/30/20 rule is a simple but efficient system for planning personal budget. Do you want to find out how to save every month? The answer comes from Elizabeth Warren, American senator and experts in economic policies, in his book «All Your Worth: The Ultimate Lifetime Money Plan». Its purpose was to provide an easy picture to be applied for ordinary people, to help reduce financial stress, without imposing impossible sacrifices.

This rule divides the monthly net profit (i.e. the amount you receive after paying taxes and taxes) in three essential categories:

50% essential needs

This category includes all the expenses absolutely necessary for daily life, without which you cannot work or survive. There are fixed and recurring costs, which must be covered with priority, regardless of the situation.

Examples of expenses that enter 50%:

- rent or domestic rate (real estate credit);

- invoices to public services (electricity, water, gas, internet);

- transport (subscriptions, fuel, car repairs);

- basic foods;

- compulsory insurance;

- basic instruction (for children);

- essential medical expenses.

The aim is to make sure that your basic needs are covered without exceeding this limit, so that there are still room for other financial categories.

Wish 30%, hobby

This category is dedicated to expenses that are not necessarily necessary, but I bring you joy, comfort or relaxation. Here are all those things that improve the quality of life, but you could lose yourself in extreme cases.

Examples of expenses in the «Wishes» category:

- exit at the restaurant or coffee;

- Holidays, travel, travel;

- clothes and accessories outside the necessary;

- streaming subscriptions;

- Courses or recreational hobbies (music, sport, painting);

- Telephone updates, gadgets or furniture;

- Beauty products, aesthetic treatments.

ATTENTION: desires are not «bad» or useless. On the contrary, they contribute to mental and emotional balance. It is important not to consume more than 30% of income.

Savings and debts of 20%

The last category, but perhaps the most important for your financial future, is dedicated to saving and debt management. This money is not for the present, but for your long -term safety and stability.

In the category 20% enter:

- monthly economies (in the savings account, mattress, in a common fund, etc.);

- Emergency fund (for unexpected situations: loss of work, medical problems);

- Refund of debt (consumption credits, credit cards);

- personal investments (actions, bonds, government securities, cryptocurrencies – depending on the risk profile);

- Private contributions for pension (pillar III, voluntary funds).

Choose balanced: savings vs investments. The goal is to create a security network and constantly work on your financial freedom.

Why does the rule 50/30/20 work?

The 50/30/20 rule is effective because:

- It offers clarity: you know exactly how much you can spend in each category;

- prevents the accumulation of unnecessary debts;

- encourages financial discipline without eliminating the joys of life;

- It helps you build healthy savings habits;

- It is easy to implement, without advanced financial knowledge.

The rule of 50/09/20 is suitable if you have a low income?

Yes, it is also suitable for people with low income, if they make appropriate changes. Is your income less than the national average (less than 3,500-4,000 do you net/month, in 2025)? Basic expenses can consume over 50% of revenues. This does not mean that you have to give up the idea, but you just have to adapt the proportions.

The goal is not perfection, but the direction. The rule of 50/30/20 should be seen as a point of reference, not as a rigid constraint. With the discipline and definition of priorities, it is possible to build a financial structure that also works for modest income.

Step by step: how the rule 50/30/20 is applied if you have a low income

Calculate your real monthly net income

Includes all sources of income: salaries, indemnities, pensions, scholarships, social aid, occasional or freelance revenues. Without a clear image, you cannot make the right decisions. For example, if you have a net income of 2,500 she per month, the classic rule would mean:

- 1,250 she for needs;

- 750 she for desires;

- 500 she for savings or debts.

Identifies essential expenses (needs)

The «needs» group includes everything that is essential: rent/mortgage, food, transport, public services, loans, compulsory education for children. Makes a clear and updated list of these expenses. If the amount exceeds 50%, it does not panic – it is a reality for many.

Here is an effective alternative to people with low income:

- 60% or even 70% for needs;

- 10-20% for desires;

- the rest for savings and debts (to avoid interests and penalties).

Regulates proportions and defines the priorities

If needs occupy 70% of the budget, it is essential:

- Reduce desires: delete or replace expensive outputs, unused subscriptions, etc.;

- Keep the savings – even minimal – 50 she a month are better than 0 she;

- Optimize fixed costs: seek cheaper energy offers, renounces expensive brands, uses discounts and vouchers.

Automatically automates

It automatically transfers a monthly amount to an income statement as soon as you receive the salary: this principle («pay yourself») works excellent for self -control.

Goals:

- creates an emergency fund (ideal: 3-6 months of essential expenses);

- Save for great planned expenses (clothing, repairs, taxes);

- Investing gradually (in mutual investment funds, private pensions, government securities, etc.).

Follow your monthly and adapted budget

Monthly monitoring is the key to success. If you use a Budget bookletA mobile application (shopping, Toshl, wallet) or an excel, you need to know:

- As long as you spent in each category;

- where you passed the budget;

- What can you adjust the next month.

Practical suggestions for low -income people

- Buy food by list and compare prices between the shops;

- Cook at home and avoid controlled food: savings can be significant;

- Reuse and repair – quality objects can be maintained longer;

- Use discounts and cashbacks – on online payments or partner stores;

- It establishes simple monthly goals – for example «this month I want to save 100 she».

The application of the rule of 50/30/20, even with a low income, does not mean giving up everything you like, but becoming aware of how you use your money. You can adapt it realistically and transform it into a tool of control and progress. With patience and discipline, you will notice visible improvements in your financial life – and not only: you will get peace, clarity and autonomy.

latest posts published

Hormones that determine financial behavior while making decisions under their influence

Payment methods Credits for consumption are getting rid of debt

Financial education for beginners – Cursvalutar.ro

What are the banking guarantees and what risks has a guarantor

Credit Bureau – Everything you need to know

Comfortable contract: taxes and exemptions

What they are and how it works

Strategies to withdraw money from investments

How to have a day without spending?